Macroeconomic impact of a commodity shock on variables monitored by central banks

The year 2026 started as a year of consolidation for the fixed income market, supported by global economic resilience and an inflation dynamic finally under control. Our baseline scenario anticipated a “soft landing” driven by Artificial Intelligence, which could act as a powerful productivity catalyst: in the United States, GDP was estimated at around 2%, with inflation expected to drop below the psychological threshold of 2% in the fourth quarter. In Europe, growth remained more subdued at 0.8%, but the rapid cooling of consumer prices towards 1.5% would have allowed central banks a more accommodative liquidity management. The outbreak of the war contributed to altering this scenario. The surge in energy prices led the market to revise the pricing of policy rates: more than one hike for the ECB and only one cut for the FED.

The outbreak of the war, therefore, had the sharp upward movement of oil as its primary effect. To attempt to estimate its impact on GDP, CPI, and policy rates, we implemented simulation models focused on various scenarios outlined by the trend of the variables monitored by central banks.

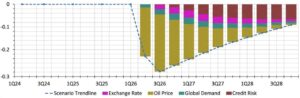

Let’s start with US GDP.

The shock appears to be -0.2% in Q2 and -0.3% in Q3 and Q4. The causes of this reduction are to be found in the combination of the increase in oil prices (simulated at 110 USD/bbl), a reduction in demand, and an increase in credit risk. On an annualized basis, this scenario would entail a total impact of approximately -1%, with 2026 GDP still remaining positive at +1%.

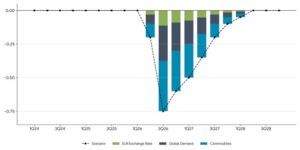

In the Eurozone, the impact would be greater, with a marked decline especially in the third quarter and a total annual impact of -1.5%, which would bring GDP to a range between -0.5% and 0%, effectively a technical recession.

Shock scenario EU GDP

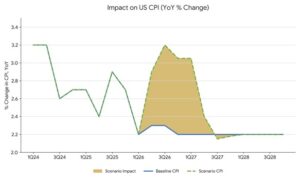

Regarding inflation, the models show an estimated increase for the United States in the 3.1%/3.2% range over the next 2 quarters, subsequently returning to the 2.1% area in the second quarter of 2027.

A similar movement is seen in Europe with a “landing” in the 2.8%/2.9% area.

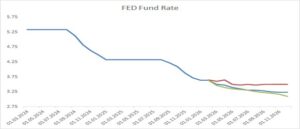

As for monetary policy in America, even in the face of the described shocks, the models do not lead to a concrete paradigm shift, with 2 cuts expected in two out of three scenarios. In the third scenario, the rate would remain unchanged throughout 2026. Obviously, the three scenarios differ based on the expected duration in quarters of the oil price shock (from 0 to 2 quarters).

In Europe, the reaction is quite similar, with a baseline scenario that anticipated a cut in the fourth quarter. In particular, it should be noted how the “recessive” effect of demand contraction prevails in the models, outweighing the inflationary effect of oil.

In conclusion, the decisive elements appear to be the duration of the conflict and, above all, oil remaining in the 100/110 area and gas above 50 euros. Even assuming an average of two quarters of commodities at these levels, the decrease in demand and consumption would have a greater impact than inflation, thus providing central banks with few motivations to raise rates. In Europe, in particular, the negative effect seems to be greater, increasing the probability of a recession.

With the rise in yields across the entire curve in this phase, the best buying opportunity in the government bond sector of the last 3 to 4 years is being created, especially in the 5/10-year segment for both core and peripheral rates.